By mid-2022, the Canadian economy had returned to or exceeded the pre-pandemic levels for most major economic indicators.

By mid-2022, the Canadian economy had returned to or exceeded the pre-pandemic levels for most major economic indicators.

In Q1 2023, TD Economics (TDE) anticipates that inflationary pressures in Canada have peaked and prices will decrease throughout 2023. Consequently, the Bank of Canada is expected to keep the overnight rate at its current level of 4.5% throughout the year. Inflation and heightened interest rates are likely to result in prolonged economic stagnation in the long term. In the short term, TDE forecasts a 0.8% GDP growth for Canada in 2023.

The British Columbian housing market remains highly responsive to increased interest rates, as the most recent data (February 2023) shows decline in the number of home sales of 49% relative to 2022’s peak levels. TDE expects government spending, increased forestry and mineral exports, and natural gas production to fuel growth. TDE’s current forecast for BC’s 2023 GDP growth is 0.6%, which has increased slightly from its Q4 forecast of 0.5%.

This post provides an update from Q4 2022 to Q1 2023 for selected economic indicators. The indicators discussed herein are both indicative and representative of the Canadian, BC, and regional economies.

Labour Market

The labour force refers to the supply (employees) and demand (employers) for labour. The number of labour force participants and the unemployment rate are indicators that highlight the material changes that took place in the labour market from Q4 2022 to Q1 2023.

COVID-19 Government Programs

The federal government initiated several programs to support employers and employees impacted by COVID-19. Currently, these COVID-19 specific programs are no longer in effect; however, the Jobs and Growth Fund no longer has COVID-19 stipulations but is available to support regional job creation in companies that meet the criteria, such as supporting the adoption of clean technology, sustainable economic growth, underrepresented groups, or the adoption of digital solutions.

National

Before the impact of COVID-19, Canada was experiencing a steady increase in labour force participants. As of March 31, 2023, the Canadian labour force comprised of nearly 21.0 million people, which is an increase of approximately 209,000 participants since the prior quarter and above the pre-COVID level of 20.0 million.

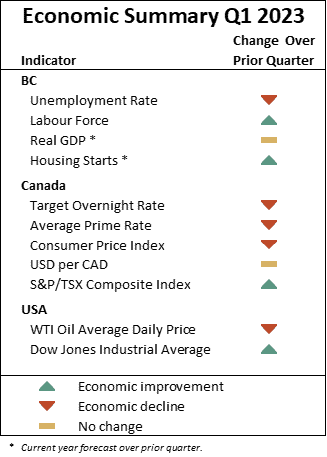

The national unemployment rate was 4.5% at the start of Q1 and finished the quarter at 5.4% which is still 0.5% lower than the pre-pandemic unemployment rate of 5.9%. However, according to TDE’s projections, Canada’s unemployment rate is expected to experience a gradual rise.

BC

During Q1, BC’s unemployment rate increased from 3.7% to 4.8%, which remains 1.2% lower than the Province’s pre-COVID rate of 5.0%. TDE forecasts BC’s average unemployment rate for 2023 to be 5.1%, which remains consistent with their previous Q4 forecast.

Regional

During Q1 2023, the unemployment rate for Vancouver Island and Coastal regions increased during from 3.0% to 3.6%, which is still 1.7% lower than pre-pandemic rates. In Victoria, the unemployment rate rose throughout the quarter from 2.6% to 3.2%, which is still trending below the pre-pandemic unemployment rate of 3.5%.

Gross Domestic Product (GDP)

National

TDE forecasts Canada’s real GDP in 2023 to grow by 0.8% for Q1, marginally more optimistic than their Q3 forecast of 3.3%. This growth is attributed to increased employment in the quarter. TDE attributes the relatively flat growth forecast to a draw-down in Canadian business inventories and a widening wedge between resilient consumer spending and reduced corporate spending.

BC

TDE forecast growth of 0.6% for 2023 for the BC economy, slightly above their 2022 Q4 forecast of 0.5%. TDE attributes this forecast to sluggish housing sales offset from increased government spending and a boost in natural gas, forestry, and mining exports.

The resulting forecast for BC’s GDP is $272.4 billion, $1.6 billion higher than 2022 and $17.2 billion above 2019, which represents pre-pandemic GDP.

Housing Market

BC

Housing starts and average residential prices reflect market indicators with a strong correlation to both the construction and real estate industries. BC’s housing starts decreased by 1.9% during 2022. The BC Real Estate Association (BCREA) forecasts a decrease in housing starts of 15.5% for 2023, followed by another decrease of 7.6% for 2024, due mainly to the slowing economy and recent interest rate increases.

BCREA forecasts a decrease of 7.1% in the BC average MLS® price for single-family dwellings for 2023, resulting in an average price of $926,000 for the year, which is a greater decrease than the Q4 decrease of 5.4% forecast for 2023.

BCREA forecast an increase of 3.1% in MLS® price for 2024, resulting in an average price of $954,000.

Regional

BCREA forecasts a decrease in average MLS® prices for single-family dwellings on Vancouver Island of 4.9% for 2023, with a subsequent increase of 2.1% forecast for 2024. In Victoria, BCREA forecasts a decrease in the average MLS® prices for single-family dwellings of 5.7% for 2023, and an increase of 1.6% predicted for 2024.

Interest Rates & Foreign Exchange

During Q1 2023, the Bank of Canada (BoC), has increased the overnight target rate to 4.50% at the end of the Q1 and the average for the quarter was 4.43%. TDE predicts that the rate will remain at 4.50% throughout the remainder of 2023 before decreasing to 3.25% for 2024 and decreasing again to 2.25% for 2025.

The rising overnight target rate resulted in an increase in the prime rate. The average prime rate for Q1 was 6.62%, which is an increase of 0.67% from the prior quarter. The prime rate will likely plateau in alignment with the target overnight rate.

The BoC has stated that it will continue to increase policy rates in an effort to return the inflation rate to the long term target of 2.00% from its recent high of 6.80% for 2022. Naturally, there is expected to be some lag in the process and TDE forecasts inflation to be 3.70% for 2023 before decreasing to 2.30% for 2024. The BoC attributes Canada’s inflation decreasing trend to lower energy, durable goods, and some service prices.

TDE forecasts the average annual USD to CAD exchange rate at $0.73 for 2023 and $0.75 for 2024. This exchange rate tends to correlate to oil prices, and over the long-term the value of the Canadian dollar relative to the US dollar typically fluctuates in-step with oil price changes.

Crude Oil Prices

Canada has the third largest proven oil reserves in the world. As a net oil exporter, the Canadian economy is heavily affected by the price of crude oil, with the greatest impact felt in Canada’s major oil producing provinces. The majority of Canadian crude oil production is in Alberta (81.0%), Saskatchewan (10.0%), and Newfoundland and Labrador (6.0%).

In North America, the West Texas Intermediate (WTI) crude oil spot price is the benchmark oil price. Historical WTI crude oil daily spot prices at the end of Q1 were:

Over the course of Q1, WTI oil prices decreased from $80.16 on December 30, 2022 to $66.61 on March 16, 2023, before finishing the quarter at $75.68. The International Energy Agency (IEA) attributes the decrease to a contraction in demand, which in turn increased oil inventories. TDE forecasts the WTI crude oil price to average $84.75 per barrel for 2023 with a further increase to $88.00 for 2024.

Capital Markets

The international response to COVID-19 at the beginning of March 2020 negatively impacted the current and anticipated operations of many privately-owned and publicly traded North American businesses. The Dow Jones Industrial Average (DJIA) and S&P/TSX Composite Index witnessed their greatest single-day percentage drops on March 12, 2020 (Black Thursday) and March 16, 2020 (Black Monday II), respectively, since the stock market crashes of 1943 and 1987.

By the start of 2021, both indices had recovered to their pre-COVID-19 levels and by the end of Q1 2022, both indices had reached all-time highs. In Q1 2023, the DJIA index ranged from $31,819 USD (March 13, 2023) to $34,303 USD (January 16, 2023). The S&P/TSX ranged from $19,379 CAD (March 15, 2023) to $20,767 CAD (January 31, 2023).

The quarter-over-quarter change was 3.7% for the S&P/TSX and only 0.4% for the DJIA. It is important to note that these indicators are based on forward-looking assumptions and analysis.

Moving into the second quarter of 2023, TDE forecasts inflation to decrease as interest rate hikes take hold and government policy continues to lower daycare costs and provide energy rebates in some provinces. The BoC expects to maintain current interest rates into the next quarter to continue to combat inflation rates that remain above their target range. As a result, projected economic growth will continue slowing through 2023 in both the US and Canada before increasing for 2024. TDE forecasts that the consumer price index will decrease throughout 2023 reaching the target range of 1% to 3% by the end of the year.

Higher input prices and labour costs are expected to continue to stifle profit margins in multiple industries. Nevertheless, energy, commodity, and food-producing sectors could continue to benefit from higher prices. TDE expects interest rates hold steady, maintaining downward pressure on housing prices.